Normal costing is a pivotal concept in the realm of managerial accounting, often employed by businesses to assess their production costs accurately. By utilizing a consistent method of assigning costs to products, organizations can gain valuable insights into their financial health and operational efficiency. This approach allows managers to make informed decisions that can ultimately impact profitability and resource allocation. Understanding the principles of normal costing is essential for businesses that aim to maintain a competitive edge in today's rapidly evolving market.

At its core, normal costing combines direct materials, direct labor, and an overhead allocation based on predetermined rates. This methodology not only simplifies the costing process but also helps in maintaining consistency across various accounting periods. By establishing a standard costing system, organizations can efficiently track variances between actual and expected costs, enabling them to respond proactively to fluctuations in the market.

In this article, we will delve deeper into the intricacies of normal costing, exploring its benefits, limitations, and practical applications. Whether you are a seasoned accountant or a business owner seeking to refine your financial strategies, this guide will equip you with the knowledge needed to navigate the complexities of normal costing effectively.

What is Normal Costing?

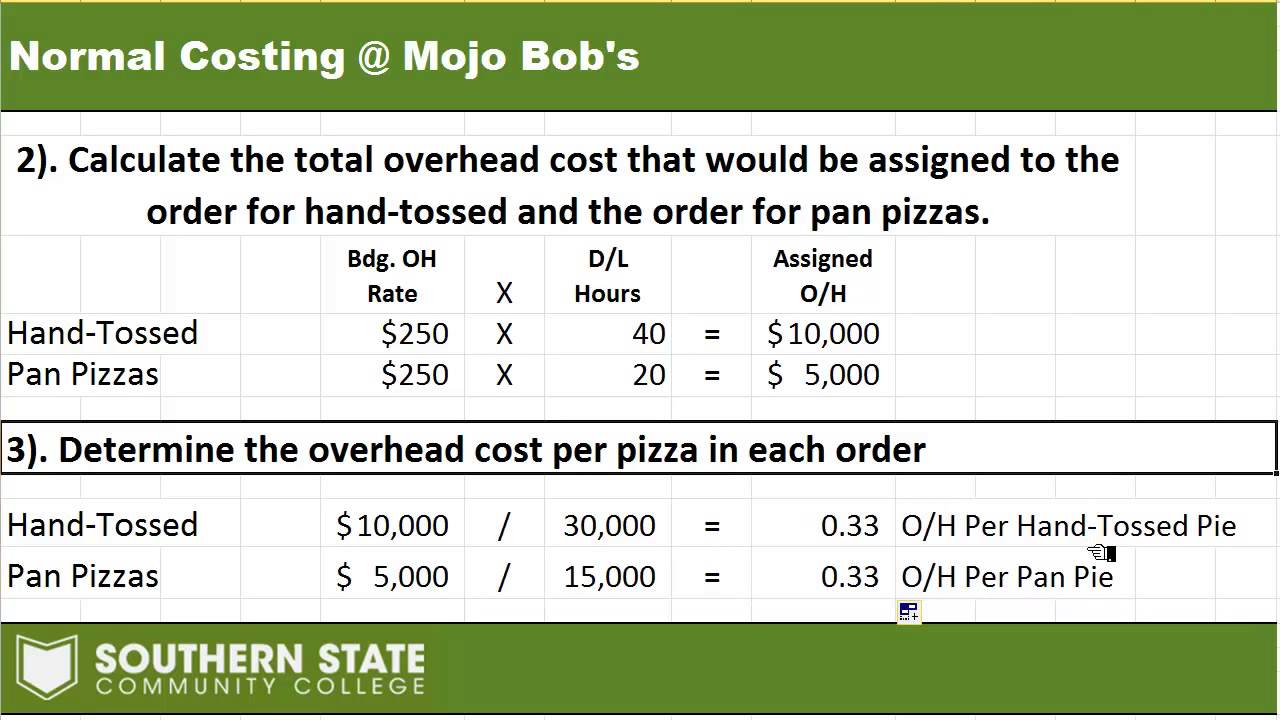

Normal costing is a method of cost accounting that assigns costs to products based on a blend of actual direct costs and estimated indirect costs. This approach allows businesses to derive a cost per unit that reflects both the materials and labor used in production, as well as a portion of overhead costs. It differs from standard costing, which relies on predetermined costs, and actual costing, which records expenses as they are incurred.

How Does Normal Costing Work?

The process of normal costing involves three primary components:

- Direct Materials: The raw materials used in the production of goods.

- Direct Labor: The labor costs directly associated with the manufacturing of products.

- Manufacturing Overhead: Allocated indirect costs, such as utilities, depreciation, and rent, based on a predetermined overhead rate.

By summing these costs, businesses can determine the total production cost for a specific period. This enables managers to set pricing strategies, budget effectively, and evaluate the efficiency of production processes.

What Are the Advantages of Normal Costing?

Normal costing offers several advantages for businesses, including:

- Consistency: By using a standardized overhead rate, companies can achieve consistency in cost measurement across different accounting periods.

- Efficiency: The streamlined process of normal costing saves time and resources compared to other methods.

- Variance Analysis: Organizations can easily identify variances between actual and normal costs, allowing for better financial control.

- Decision-Making: Accurate cost information aids management in making informed pricing and production decisions.

What Are the Limitations of Normal Costing?

While normal costing has its benefits, it is not without limitations. Some of these include:

- Estimation Error: The reliance on predetermined overhead rates can lead to inaccuracies if estimates are not regularly updated.

- Less Flexibility: In rapidly changing environments, normal costing may not reflect the true cost of production accurately.

- Overhead Allocation: The method of allocating overhead may not accurately represent how resources are consumed in production.

How is Normal Costing Used in Business?

Normal costing is widely used across various industries for multiple purposes, including:

- Cost Control: Monitoring and controlling production costs to enhance profitability.

- Budgeting: Developing budgets based on historical normal costs to project future expenses.

- Performance Evaluation: Assessing the efficiency of production processes by comparing normal costs to actual costs.

- Product Pricing: Establishing competitive pricing strategies based on accurate cost information.

Can Normal Costing Be Integrated with Other Costing Methods?

Yes, businesses can integrate normal costing with other costing methods to enhance their financial analysis. For example, combining normal costing with activity-based costing (ABC) allows organizations to gain a more nuanced understanding of their cost structure. By analyzing costs at a more granular level, businesses can identify areas for improvement and optimize their operations.

Conclusion: Is Normal Costing Right for Your Business?

In conclusion, normal costing is a valuable tool for organizations seeking to manage their production costs effectively. By understanding its principles, advantages, and limitations, businesses can make informed decisions that contribute to their overall success. Ultimately, the choice of whether to implement normal costing should be based on the specific needs and circumstances of the organization.

As you consider adopting normal costing, evaluate your current costing methods, assess your business environment, and determine how this approach can fit into your overall financial strategy. The insights gained from normal costing can lead to improved operational efficiency, better pricing strategies, and ultimately, enhanced profitability.

How To Make Your Door Close Slower: A Comprehensive Guide

Embracing The Heart: Understanding Sentimental Significance

Unveiling Madison's Diary House Party: A Night To Remember